Notre objectif est de mettre en partage sur nos trois spécialisations (stratégies et management de l'innovation business tous secteurs, stratégies de croissance ENERGIE et CLEANTECH, stratégies de croissance DIGITAL),

les analyses d'Innhotep, celles de nos invités et des articles tiers issus de notre veille.

Accélérateur d' "innovations business", Innhotep intervient comme conseil auprès de grands groupes et accompagne le développement de start-up high-tech.

Des chercheurs du Fluid Interface Group au MIT Media Lab ont développés une bague qui permet de scanner un texte pour le lire à voix haute.

Dans un monde où les individus lisent et s’informent de plus en plus sur des supports numériques tel que les liseuses Kindle et tablettes, les personnes malvoyantes se retrouvent fortement désavantagées. Mais un nouvel outil qui lit à voix haute n’importe quel texte devrait bientôt permettre aux personnes aveugles d’obtenir une vaste quantité d’information du bout du doigt, sans avoir besoin d’un texte en braille. Le dispositif nommé FingerReader, vise à remplacer les logiciels audio-visuels qui peuvent se révéler être assez limités et inexactes. Développé parFluid Interface Group au MIT Media Lab (laboratoire de recherche duMassachussetts Institute of Technology), dans le cadre d’un projet global de réduction du fossé entre le monde digital et le monde réel, cet outil s’adresse aussi bien aux personnes ayant une déficience visuelle qui ont besoin d'aide pour lire un texte imprimé, qu’aux individus qui souhaitent traduire un texte et apprendre une langue.

Un assistant de lectureLe prototype FingerReader permet à son utilisateur de scanner les lignes d’un texte avec son doigt et de recevoir un retour audio sur les mots. Le lecteur suit les lignes de texte avec son index, de la même façon qu’il pourrait le faire en lisant réellement. Une camera est intégrée dans la bague située et une voix imitant celle de Stephen Hawking, physicien théoricien et cosmologiste britannique célèbre, répète à voix haute les mots scannés. Il fournit également des informations de mouvement, sous la forme de petites vibrations pour prévenir l’utilisateur lorsqu’il s’éloigne du texte ou lorsqu’il saute des lignes. De plus, le wereable serait capable de traduire le texte dans une autre langue.

Créer des dispositifs intuitifs et éducatifsLe FingerReader aurait été élaboré suite à un premier concept élaboré par le MIT Media Lab, suivant l’objectif de créer des dispositifs plus intuitifs. En 2012, ce projet nommé EyeRing, correspondait à une caméra connectée en Bluetooth, montée sur un doigt, qui permettrait de saisir un texte pour le transférer sur un Smartphone ou une tablette afin d’être lu de nouveau à l’utilisateur. L’objectif était non seulement d’aider les malvoyants à lire des signes et étiquettes mais aussi à aider les enfants à apprendre à lire. Le dispositif FingerReader est toujours en phase de développement, et certains éléments sont encore à améliorer. Par exemple, la vitesse de lecture est plus lente que ce qu’elle pourrait être et des écouteurs pourraient être installés afin de réduire le bruit ambiant et produire une meilleure audibilité. Les chercheurs du MIT envisagent aussi que ce dispositif permette aux individus d’apprendre une nouvelle langue.

The WhatsApp figures are startling: $4bn of cash, $12bn in Facebook shares and a further $3bn in stock that will vest over the next few years. Photograph: Justin Sullivan/Getty Images

People will bring their prejudices to the table when judging whether Facebook agreeing to pay up to $19bn for messaging app WhatsApp is a smart deal or not.

Some will see it as the latest evidence of a froth-fuelled social networking and apps bubble, which won’t end well. Others will hail it as the bold, decisive move of a visionary CEO.

WhatsApp may be labeled as the next Myspace or Bebo: bought for big bucks then withering as its users drain away. But it may also be seen as the next YouTube – bought for what seems like a ridiculously high sum, only to thrive so well that price looks like a bargain a few years down the line.

As with any big technology story, people will fit Facebook’s WhatsApp acquisition neatly into whatever their existing narrative is for what’s happening around smartphones, social networking and big tech more generally.

Nevertheless, here are some facts and expert views to help you draw your own conclusions about the impact of the deal.

Multiple Facebook apps in your home screen

When the deal closes, Facebook will own four of the world’s most popular smartphone apps: Facebook itself, Instagram, WhatsApp and Facebook Messenger – the social network says it’s committed to maintaining the latter, although we’ll see if that holds true in the long term.

Facebook wants to be on your smartphone in multiple ways, taking up several slots on your homescreen rather than just one. This strategy had already been outlined before yesterday’s news, though.

“Our vision for Facebook is to create a set of products that help you share any kind of content you want within the audience you want. We’re not just focused on improving the experience of sharing with all of your friends at once,” CEO Mark Zuckerberg told analysts during Facebook’s last earnings call.

“One of the things that we want to try to do over the next few years is build a handful of great new experiences that are separate from what you think of as Facebook today.”

If the average person’s smartphone usage tilts towards using a group of apps that mostly do one thing well – messaging, photos, games, whatever – then Facebook wants to be providing as many of them as possible. And if it can’t build successful enough standalone apps, it will buy them.

Look beyond the dollar amount

The figures are startling: $4bn of cash, $12bn in Facebook shares and a further $3bn in stock that will vest over the next few years. Cue the obvious “How many X is WhatsApp worth?” calculations – 19 Instagrams, 76 Washington Posts, or 96bn extra moves in Candy Crush Saga – which might even be enough to get you past level 147.

It’s important to look beyond the pure dollar amount, though. The former mobile analyst Benedict Evans, who now works for venture capital firm Andreessen Horowitz, thinks it’s more useful to think about the impact on Facebook using other metrics.

“It paid first 1% of its market value for Instagram and now close to 10% for WhatsApp, taking not dominance but at the least two of the commanding heights of mobile social,” he wrote in a blog post after the news was announced.

“That’s the right way to think about value, I think - not ‘OMG $16bn!’, but ‘is this worth 10% of Facebook?’ The deal values WhatsApp users at $35 each (very close to what Google paid for YouTube, incidentally), but the current market cap of Facebook values its MAUs at $140 or so.”

The entrepreneur and investor Martin Varsavsky also addressed the valuation of WhatsApp in his own blog post.

“The WhatsApp acquisition price sounds high, sky high, crazy high. But it’s not if you put yourself in Zuckerberg’s shoes and think about it in these terms: Facebook bought a network that is growing much faster than itself (growth drives valuations) and has almost half as many members already, for 10% of its value,” he wrote.

“So from this perspective it is reasonable to pay that price. If you call WhatsApp a better SMS system, on size alone, it is as big as half of all the texting that goes on in the world. SMS as Facebook said in its investor conference after the acquisition is a $100bn industry although imploding fast to the tiny cost of WhatsApp, $1 a year.”

Forrester’s Julie Ask suggested that the deal is an example of pragmatism on both sides. “There are a dwindling number of privately held companies with audience numbers in the hundreds of millions. Tencent (WeChat) is public. Line belongs to Naver Corporation. Rakuten bought Viber last week,” she wrote. “Kudos to the founders for not snubbing a few billion dollars.”

No ads, maybe, but…

Facebook bought Instagram, waited, then introduced advertising. WhatsApp will go the same way, right? Actually, wrong, according to its CEO Jan Koum. “Here’s what will change for you, our users: nothing. WhatsApp will remain autonomous and operate independently,” he wrote yesterday.

“You can continue to enjoy the service for a nominal fee. You can continue to use WhatsApp no matter where in the world you are, or what smartphone you’re using. And you can still count on absolutely no ads interrupting your communication. There would have been no partnership between our two companies if we had to compromise on the core principles that will always define our company, our vision and our product.”

WhatsApp’s no ads policy has been consistent throughout its rapid growth to 450 million active users: its business model settled down as a $1 annual subscription after a year of free usage. Can that stance really survive once WhatsApp is part of Facebook?

Two points. First: WhatsApp has huge reach but it doesn’t really have enough data to be really interesting for advertisers in its current form. By design; it doesn’t collect names, ages, genders or addresses, and it doesn’t store users’ messages on its servers. Not a great ad-targeting platform compared to the way Facebook’s advertising business works.

Second, though: what WhatsApp does collect is people’s phone numbers. An alternative way of looking at the deal is as Facebook agreeing to pay up to $19bn for 450 million people’s phone numbers – more, if you consider registered users rather than active ones.

“Lot of info in a phone number. Tie it all back to everything else. Ick,” as one industry source told the Guardian. Will all those phone numbers help Facebook’s advertising business outside WhatsApp? That’s a question to ponder in the months ahead.

Facebook bought the simplest messaging app

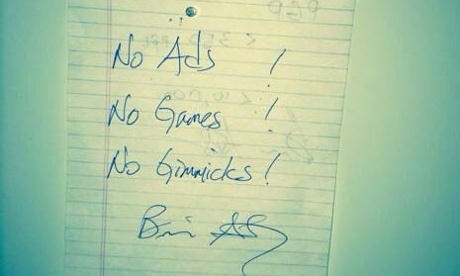

A Tumblr post by WhatsApp investor Jim Goetz, of VC firm Sequoia, includes a photograph of the note stored on Koum’s desk – a three-line statement of WhatsApp’s guiding principles written by his co-founder Brian Acton:

The ethos behind WhatsApp. Photograph: Jim Goetz

Most of WhatsApp’s rivals – from Line, Kakao and WeChat in Asia to Kik and BBM in the west – have been turning themselves into platforms for everything from gaming and music through to shopping and brand marketing. In a sense, they’re all trying to replace Facebook, in a sprawling, multipurpose sense.

WhatsApp is for messaging. No games, and no gimmicks. And it’s the app that a) got to 450 million active users, and is still adding 1 million a day in 2014, and b) got bought by Facebook for up to $19bn. Its single-minded simplicity is what made it worth so much in Facebook’s eyes.

Expect frenetic speculation about which messaging apps will get bought up next, by which tech giants for what purpose. Naturally, some of these companies will be eagerly fuelling the speculation.

“It’s $16bn clearer that we’re now in the age of the mobile messenger,”Kik’s CEO Ted Livingston told TechCrunch last night (referring to the initial cash-and-stock price Facebook is paying). “Having a popular mobile messenger is simply going to become table stakes for competing in the mobile era.”

There will be consolidation – of course there will – but it’s less about “company X is now worth Y because WhatsApp was worth Z” and more about what specific messaging apps are worth to specific buyers. Simplicity sealed the deal for Facebook, but will the mini-Facebook platform strategy tempt others?

“From an industry perspective, it is likely that further consolidation will occur, though it’s unlikely that subsequent acquisitions will provide as high a return as that achieved by WhatsApp,” said the Informa Telecoms & Media analyst Pamela Clark-Dickson today.

Meanwhile, Forrester analyst Nate Elliott has warned against seeing the deal as Facebook chasing teenage users who may have drifted away from the social network. “It’ll be tempting to read this as a sign Facebook is scared of losing teens. And yes, the company does have to work hard to keep young users engaged,” said Elliott.

“But the reality is, Facebook always works hard to keep all its users engaged, no matter their age. Facebook is tireless in its efforts to keep users coming back. That’s why their 1.2 billion monthly users keep visiting the site more and more frequently, rather than drifting away.”

Hello operators

Zuckerberg’s next public appearance is a keynote speech at the Mobile World Congress conference in Barcelona later this month: an event still dominated by the global mobile operators.

Imagine if Zuckerberg had saved the WhatsApp news for a one-more-thing moment towards the end of his speech. “Facebook is a strong partner for carriers, not their enemy. We complement their business, not cannibalise it. Oh, by the way, we’re buying WhatsApp …”

It’s difficult to avoid viewing the acquisition through the prism of what it means for the wider telecoms industry, at a time when WhatsApp and its rivals have already done a good job of surpassing the volume of SMS text messaging. It’s not so long since the prospect of a “Facebook Phone” was seen as a threat to operators. Now think about Facebook owning phone messaging.

“Mobile operators are in an interesting position: Facebook, one of their key content partners, now owns an application that has been a major catalyst in the decline of SMS revenues and, for some, SMS traffic,” said Clark-Dickson.

Varsavsky thinks the social network has more ambitious plans than that. “Where are Facebook/WhatsApp headed? In my view to do with telephone minutes what WhatsApp already did with SMS,” he wrote.

“It is surprising that Facebook which wants to connect everyone on the planet still does not have a platform to people to have actual conversations a la Viber or Skype. I can’t imagine that things will stay this way. And owning world’s texting and world’s conversations may very well be worth $19bn.”

Evans takes a different view, highlighting the stats comparing mobile messaging apps’ growth to SMS texting volumes, while suggesting that the potential of something like WhatsApp lies beyond pure communication.

“Mobile social apps are not, really, about free SMS. Mobile discovery and acquisition is a mess – it’s in a ‘pre-pagerank’ phase where we lack the right tools and paths to find and discover content and services efficiently,” he wrote.

“Social apps may well be a major part of this, as I discussed in detailhere. These apps have the opportunity to be a third channel in parallel to Google and Facebook.”

The company’s Power Sleep app harnesses the computational power of the devices to crunch cancer research data at a time when they’re otherwise not in use.

Considering how useful smartphones are, there’s still plenty of untapped potential.Locket has already gone some way to earn smartphone owners cash by turning their lock screens into ad space, and now a new app called Power Sleep harnesses the computational power of the devices to crunch data at a time when they’re otherwise not in use.

Cancer researchers at the University of Vienna find themselves with masses of protein data that they can’t sift through themselves — instead, they rely on computers to process it over long periods of time. To get the job done more quickly, the Power Sleep app developed by Samsung Austria is hoping to crowdsource computing power from the processors inside people’s smartphones. Many already use alarm clock apps that require their phones are kept running throughout the night and Power Sleep doubles as a replacement for those apps. Users simply set the alarm and the phone then begins to collect packets of data containing protein sequences from the university, compares them, and sends the results back to the lab. Currently available only for Android, the app is free to download from Google Play. The video below offers some more details about the app:

Power Sleep is similar to existing projects such as Stanford’s Folding@home and UC Berkley’s BOINC, whose technology the app is actually based upon. Are there other projects that could utilize the combined power of otherwise idle smartphone networks?

Sprinkling some big-data sauce on sales or marketing software won’t get a dime out of these moneybags.

Four prominent venture capitalists who have funded big-data companies dished about what they’ve gotten tired of — and what they might actually like to fund — at O’Reilly Media’s Strata big-data conference in Santa Clara, Calif., on Wednesday. The talk brought nuance to the hype-filled big-data aisle of the IT market.

“The most grotesquely overinvested category I have seen is anything that has to do with sales and marketing,” said Matt Ocko, the managing partner at Data Collective.

That includes taking marketing-automation software like Marketo or customer-relationship management software like Salesforce.com and adding some natural-language processing on top to analyze and pull useful information out of plain text from other sources. Or adding in some artificial intelligence, for that matter.

Also, Ocko said, you can’t be doing what a bunch of other people have already done. To use Ocko’s words, if you want to get funded, don’t be “the eleventh [person starting] a Wi-Fi chip company, the fourteenth [person doing] scale-out storage.” It’s probably not going to work.

That also goes for companies interested in building commercial distribution of the Hadoop ecosystem of technologies for storing, processing, and querying lots of different kinds of data. “Anyone besides Cloudera is doomed,” Ocko said, referring to a company that’s in a position to go public this year.

Jake Flomenberg, a partner at Accel Partners, said he’s got some reservations on startups that use machine-learning algorithms that can provide more accurate or useful results over time as more data becomes available.

“I think the disconnect that I far too often see is that people are focused on the technology in and of itself, more than the direct use cases,” Flomenberg said.

Plus, he said, the market size might not be large. “Not only are you selling to a data scientist, you’re selling to a data scientist with a really big, gnarly data set, [using the] Random Forest [algorithm] or a type of linear regression,” he said.

“To the rest of the world, they have no idea what to do with this tool.”

Roger Chen, an investor at O’Reilly AlphaTech Ventures, worries that some startups pushing devices with data-generating sensors “have no clear pathway toward being part of any bigger system later on.” That could mean the data stays within the realm of a wearable device’s application and never becomes available for integration with other sorts of data. So the number of interesting outcomes based on the data is limited.

Ross Fubini, a venture partner at Canaan Partners, thinks business-intelligence software for analyzing and asking questions of data are “undifferentiated too often.” And it’s not just a matter of making “prettier widgets or prettier toolsets,” Fubini said.

Mobile, insurance, and more

If anything, Fubini said, startups might be able to capture funding by building technology that enables compelling user experiences on mobile devices.

And it sounds like specific industries could benefit from some new applications that draw on big data.

Chen pointed to the insurance industry. And he called out health-specific applications like finding connections between disease outbreaks and weather patterns.

Despite Ocko’s disinterest in applying big data techniques to sales and marketing tools, Flomenberg cited software for salespeople — specificallyRelateIQ — that’s much can pull in data more easily more traditional customer relationship management (CRM) tools like Salesforce.com.

“They turn a tool that people can’t stand to live with to one they can’t live without,” Flomenberg said.

Tools that can help data scientists save lots of time, such as Trifacta, which simplifies the process of getting a big heap of data ready for analysis, can also be appealing.

In fact, Flomenberg’s firm is an investor in both Trifacta and RelateIQ.

As for Ocko himself, he likes “idiot savants” trying to solve targeted problems in “narrow categories” that could result in the “complete overturn of everything in the existing quarter.”

Moleculo, one startup Data Collective invested in, found a way to pull critical signals from genetic sequencing data “better than anything else we have ever seen.” Illumina ended up acquiring Moleculo in 2012.

But these categorical generalizations can fall away, Fubini said, “when applications have that feeling of magic.” Take Amazon’s way of telling you what you want and then getting you to buy it.

“The applications that we don’t see — the technology behind it — that’s the stuff that’s going to be interesting to me,” he said.

The IoT community is still debating which of three different funding models will best support development, with some favored by Europe and some by the US. Understanding these models is crucial to understanding where the technology is heading and what region will lead the way.

When it comes to smart cities and the internet of things, everyone asks, “Where is the money?” I have observed very dissimilar points of view on financing for the IoT in keynote topics in conferences and in discussions throughout the year, in particular at the recent Internet of Things Forum in Cambridge in the U.K., and the M2M & Internet of Things Global Summit in Washington D.C. It struck me that the ideas were as far apart as the venues themselves. It’s important to understand these different funding models, because they are driving the development of the IoT.

There is no easy answer to the funding question because the IoT market is still very fragmented. From our perspective of sensors and hardware, we see small pieces of revenue coming from many different verticals. I think of these as trial balloons, just validating the huge potential of the IoT and its power to be the next technology revolution. Even so, we see smart agriculture and smart cities as the verticals with the most traction right now. Differences in these two sectors shed light on the key question of funding the IoT. Will it be public or private?

The three primary funding models

Smart agriculture is privately funded in many cases, and the return on investment has to be obvious from the start. Smart cities have so many more stakeholders and the approach is not so clear-cut. There are many different ways to support their development, some coming from academia, communities, and industry.

1. Public money. In my view, had it not been for the economic crisis, public funding would have been the normal route. Right now European Union funds play an important role in allowing a number of connected smart cities pilots to really test the technology and accelerate the uptake of services. The existence of these European Commission funds makes the difference between what we see happening in Europe vs. the US market, allowing Europe to lead the way.

At Cambridge people thought of Europe as ahead of the U.S. in the IoT, whereas in Washington there were fears that a “go-with-grants” model is harmful because it is an unsustainable business model. The U.S. wants to see how Europe will maintain smart cities projects over time, and several critics point to the lack of a business model in flagship smart cities projects funded with EU funds. It’s true that these projects are usually led by academia, and business sustainability is not usually the focus. But don’t forget: the very first step is validating the technology.

2. Public/private partnership (PPP). In PPP, private companies invest and go on a cost-savings-share model with municipalities. It is a viable funding mechanism for smart cities, and in fact, the US has a history of finding capital for transportation and infrastructure projects this way. PPPs can create new forms of cooperation and resource sharing.

In this model, who would be the perfect private partner? Here, we stumble into a paradox in the nascent IoT market. Due to the similarity between IoT networks and telephony networks, operators should be the logical owners of IoT infrastructure as a new connectivity channel. However, the system integrators are the ones leading the way. This is because an operator needs to cover a whole country, or at least a circuit including major cities, and that requires a lot of investment. On the other hand, integrators can jump from project to project, testing the hottest verticals. But keep your eye on the bouncing ball, because this situation is evolving. Today operators are letting the integrators pay for their education.

3. Citizen participation. Community-led projects that apply the current trend of crowdfunding through platforms like Kickstarter are gaining momentum. I know of a number of civic projects that are spearheaded by citizen activists, such asAirQualityEgg, a device that measures air quality, or SafeCast’s network of individual airborne radiation sensors in Fukushima (Libelium was a partner in this project).

SafeCast’s crowdsourced map of airborne radiation in Japan.

This is such an interesting model, and I wonder if governments can incentivize citizens to acquire the sensors and build the systems themselves, perhaps by offering tax breaks or other benefits.

Investing the funds: hardware or services?

Once the money is raised, how will we spend it? In Cambridge, the prevailing view was that IoT money should be devoted to infrastructure. In Washington D.C. people were not so sure, because they believe in a model where services generate more money than hardware.

For the sake of argument, I like to compare the IoT to the railway age. There are many parallels, not only because both of these inventions are industrial revolutions with the ability to change everything. For a moment, try to imagine railway and train builders pitching to raise money. Would venture capitalists just tell them “Nah! We prefer to invest in companies that will be handling the ticketing system…?” Of course not! No services are possible, nor is any other type of future business, if we do not have the infrastructure in place.

Someday, it is true, hardware will be commoditized, and revenues will come from services associated to data, but if we are in the midst of raising a new market, that day is still really far away.

Alicia Asin is the co-founder and CEO of Libelium, a provider of open hardware for wireless sensor networks used in Smart Cities and Internet of Things projects.

While well established startup markets outside of Silicon Valley such as New York, Boston, and Seattle are already on venture investors’ radars, a key market for technology investment opportunities that has often been overlooked is Canada and its tech hubs, including Toronto, Waterloo, Vancouver, and Montreal.

Over the past five years, significant changes have taken place in the country’s technology ecosystem and regulatory environment. They have fueled a new era of innovation, nurturing standout companies like HootSuite, Kik, and Indochino and making Canada a key market to watch.

Where Canada is leading

What makes many Canadian technology startups so attractive to investors is that the companies have sustainable business models, with real revenue and a focus on solving very large, albeit sometimes unsexy, problems.

Material exits of globally recognized Canadian technology companies have occurred over the past few years — Eloqua to Oracle for $871 million, Taleo to Oracle for $1.9 billion, and Radian6 to Salesforce.com for $326 million, among others –- with minimal awareness that these were all Canadian-founded companies.

Canada is home to many quickly growing Software-as-a-Service companies like Vidyard, a Y Combinator alum, and FreshBooks, in addition to e-commerce players such as Kobo (acquired by Rakuten for $315 million), Beyond the Rack, and Frank & Oak. Desire2Learn and TopHat are disrupting the education market, and companies like, Shopify, BuildDirect, and Tulip Retail are disrupting retail infrastructure by creating new technology platforms and data-enabled distribution systems. Software-enabled hardware startups like Bionym and Thalmic Labs are leveraging the software-enabled hardware talent from Nortel and BlackBerry to create innovative devices and services.

In fact, the recent decline of BlackBerry has released a plethora of talent –- experienced technology executives and junior engineering talent alike –- into the Canadian tech ecosystem. The fall of this one giant will plant the seeds for hundreds of others to grow.

Home-grown tech talent

Conventional wisdom in Canada held that once you were ready to scale your company, you needed to move to Silicon Valley, or just get acquired by a larger technology company.

However, that dynamic is rapidly changing, and Canada is now seeing large American technology companies setting up shop to take advantage of the country’s rich engineering talent, lower operating costs, and thriving entrepreneurial ecosystem. For example, Facebook, Amazon, Google, Twitter, and Square all have offices in cities such as Vancouver, Toronto, Waterloo, and Montreal. The presence of these world leaders in technology in Canada injects additional energy and seasoned, as well as cutting edge, expertise into the startup ecosystem.

Canada is world-renowned for its high-quality post-secondary education, with the University of Waterloo’s engineering co-op program at its core. In fact, the Waterloo area is also now home to the Perimeter Institute, a globally recognized leader in theoretical physics graduate studies and research. And while Canada has always churned out top engineering talent, today it’s also producing outstanding technical entrepreneurs.

A friendly business environment

Many of the developments in Canadian technology wouldn’t be possible without several new initiatives. One of the most important changes was the removal of Section 116 from the tax code in 2009. The Section 116 change was significant because it made a startup investment much less complex and costly for U.S. investors.

Now foreign technology venture funding, represented largely by the U.S., is flowing into Canada in large amounts. In fact, the C100, the leading Canadian technology entrepreneur association in North America, has seen more than $700 million of U.S. venture dollars invested in Canadian technology companies involved in its ecosystem over the past couple of years.

In 2013, Canada took a bold stance when it announced its Startup Visa Program. A billboard in Silicon Valley enticed with “Pivot to Canada” –- a campaign aimed at attracting foreign entrepreneurs to Canada -– and a bit of a poke in the eye to the U.S., which has struggled to pass its own startup visa program.

R&D tax credits and refunds unique to Canada help to lower the cost of starting a company. Michael Litt, the founder and chief executive of Vidyard, says that by his estimates, it is up to two-thirds less expensive to start and run a technology company in Canada versus Silicon Valley. A number of his Y Combinator cohort companies weren’t able to get nearly as far along with their businesses as he did, given the expense and competition for talent in Silicon Valley.

There is also a new generation of talent that is helping to build the startup ecosystem in Canada. Iain Klugman and his team have built Communitech in Waterloo, a massive technology hub that supports more than 700 startups and several global technology companies, along with a couple of incubators and an accelerator. And smart, driven early-stage investors like Boris Wertz of Version One Ventures, J.S. Cournoyer of Real Ventures, and Chris Arsenault of iNovia Capital, among others, have all helped to raise the bar of what success should look like for Canadian technology entrepreneurs.

Heads up, keep an eye on your northern neighbor

Canada is a tech hub worth keeping your eye on over the coming year. There’s a new generation of technology entrepreneurs dispelling the stereotype that Canadians are “too nice” to aggressively do what it takes to build a billion-dollar company.

Mike Serbinis, chief executive of Kobo, identifies with Canadian technology entrepreneurs being scrappy risk takers. He said that he feels akin to Peter Munk, who started a mining company in the middle of nowhere in Canada and built what is now the largest gold mining company in the world, Barrick Gold. Peter was a Hungarian immigrant to Canada, and a true entrepreneur who took real risks and made huge bets. As Mike sees it, Peter’s tenacity is the closest thing he can compare to what he’s done to build Kobo, which is now doing over $1 billion in revenue.

With the thriving ecosystem and regulatory groundwork developed over the past five years, along with a set of scrappy and talented technology entrepreneurs, Canada is poised to see a groundswell of category-leading technology companies emerge on the global stage in 2014 and beyond.

Katherine Barr is a general partner at Mohr Davidow Ventures and a co-chair of the C100, the leading Canadian technology entrepreneur association in North America. On Twitter, find the C100, Katherine, and Mohr Davidow.